Time Series Analysis

Tags: Fintech

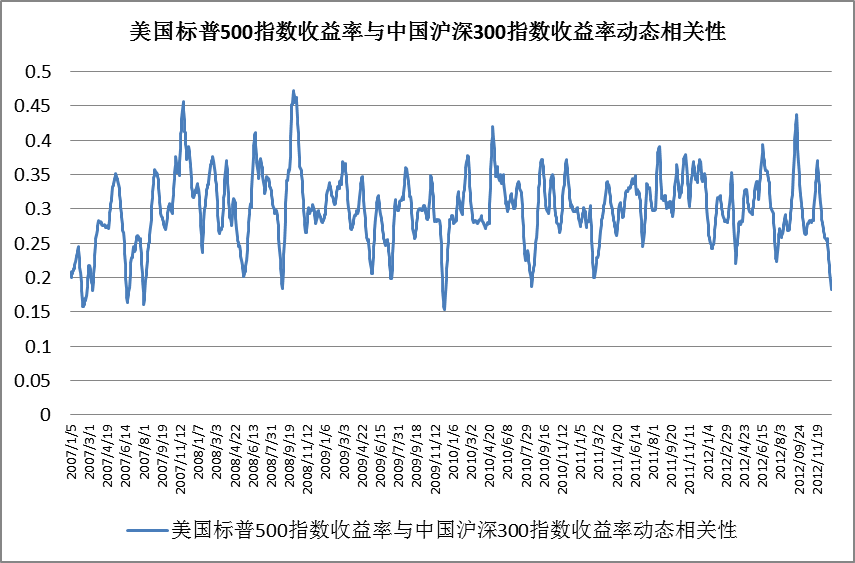

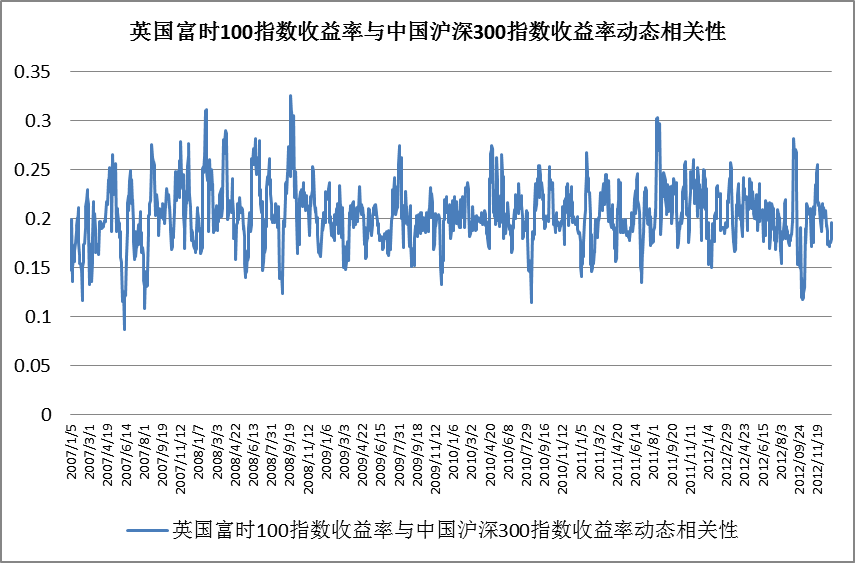

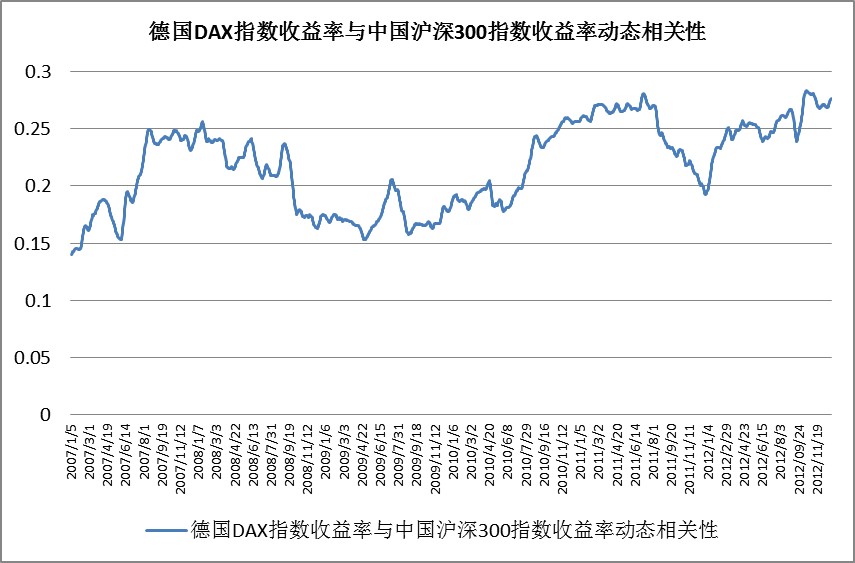

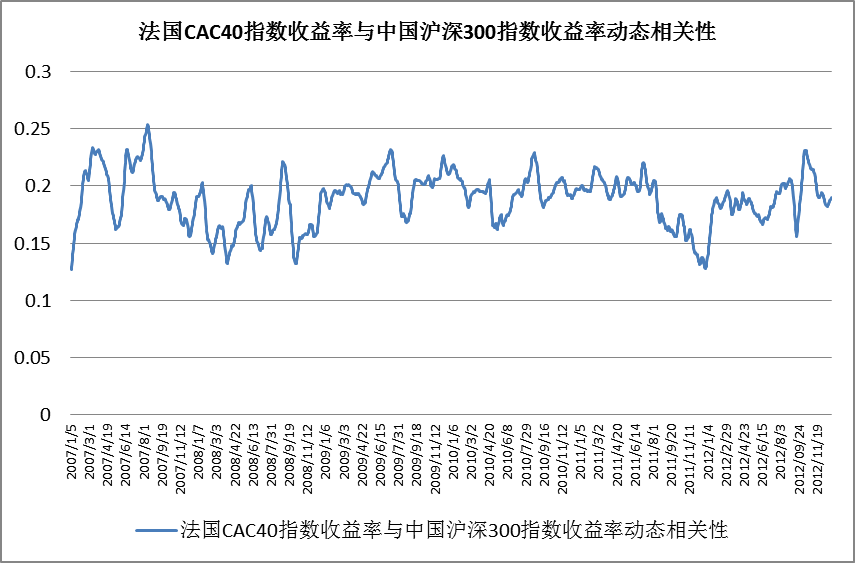

This is from my PhD disertation. I did some research on the linkage between global financial market and Chinese stock market with time series analysis methodology.

The Copula model is used to study the linkage. It can be described in two steps:

- For each financial market, I first estimate the F distribution, which I used the GARCH model.

- estimate the multiple joint distribution with Copula model